The Hard Insurance Market is upon us and premiums are rising…

The real question is, what is the true cost of insurance?

We all want insurance costs to remain flat or go down, but the truth is, rates are going up.

However, do you know what is included in your insurance premium? Here is a simple breakdown of your insurance premiums:

- Fronting Costs

- Reinsurance Costs (specific and aggregate)

- Claims Handling Costs

- Loss Control Costs

- Other Administrative Costs

- Legal

- Actuarial and Accounting

- Management Expenses

- Claims Fund

Only the Reinsurance Costs (specific and aggregate) are “pure insurance.“… The “balance” of the premiums are Administrative Costs and your Claims Fund.

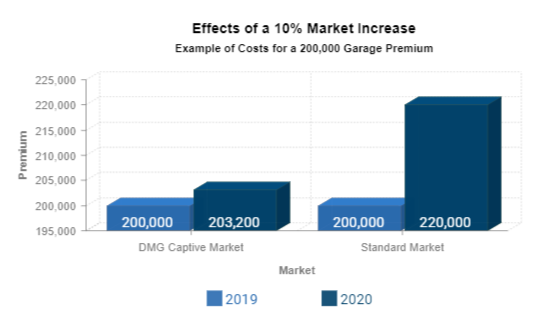

Let’s examine the effects of a 10% market increase on a Captive vs. Standard Program:

When your Insurance Company increases your premiums by 10% – 15%… they are actually increasing your cost by much more than that… increasing all of the claims handling, administrative costs, AND your Loss Fund (which they keep). All under the “guise” of a small increase. You can see by the graph below what a difference this makes.

Take control of your insurance costs… stabilize your premiums with a true Loss Sensitive program. Secure a Return of Underwriting profits from those good years. At Dealer Management Group we believe there should be total transparency in what you’re paying for – view our Annual Report and Premiums Breakdown.

It’s time to discover the Captive, Dealer Management Group (DMG). DMG offers a level of stability and control not available by the standard Garage and Workers Compensation Marketplace. Take our Questionnaire to see if your Dealership qualifies for the Captive.